By: Navid Ladani

For decades, property buying has followed the same emotional script: fall in love with a showroom unit, scramble for financing, and hope the numbers somehow work out. Faizul Ridzuan, CEO of FAR Capital, believes this model is fundamentally flawed. Instead of starting with properties, his company starts with people – screening buyers’ financial profiles first and using data to engineer demand before supply even hits the market.

The result, he suggests, is significantly higher loan approvals, faster sales, and properties secured at prices lower than traditional retail levels. In this interview, Ridzuan goes into why real estate should be treated as a financial engineering problem, how bulk “community buying” can potentially unlock wholesale pricing, and why emerging Southeast Asian markets appear to offer the perfect testing ground for this model.

Q: FAR Capital positions itself as starting with financial screening rather than property selection. Why did you design the business around filtering buyers first, and what does this approach reveal about how most people misunderstand property affordability?

Faizul Ridzuan: “We flipped the model because the old way does not seem to work well. Instead of pushing supply, we focus on analyzing actual demand using data. This lets us show developers exactly where their product stands and the price point needed to achieve sales. Most people buy on emotion, falling in love with a showroom unit, only to get rejected by the bank weeks later. That’s not investing; that’s heartbreak. For developers, it’s a costly waste of time. When we flip the script, the results can be dramatic: our loan approval rates are nearly 150% of the market average, and our booking conversion hits 80%, double that of most new launches from other agencies.

At FAR Capital, property acquisition is a financial engineering problem. The issue is the gap between what people want and what they are eligible for. You might afford the monthly payment, but if your credit profile is messy, the bank says no. We built our business around screening. You can run fast, but it’s useless if you’re running the wrong way. Our data also lets us predict exactly which assets a client needs for the next five years. The endgame? An automated predictive model that maps a client’s entire financial lifecycle, starting with property and expanding into every other financial vertical.”

Q: Your “data-aggregated community buying” model suggests securing properties 20–30% below market price. What market inefficiencies make this possible, and why haven’t developers or traditional brokers solved this problem themselves?

Faizul Ridzuan: “The inefficiency that allows FAR Capital to thrive is when the market has an oversupply situation, when developers build products without the right data, and when there is a gap between affordability, needs, and supply. Most of the current players are not truly data-driven, or worse, they rely on the wrong data to predict demand. Even a proptech giant like Zillow lost nearly $600 million in a single year trying to play this game. They failed because their algorithms used the wrong assumptions; they aggressively acquired supply by overpaying, artificially driving prices up, only to get crushed when the market cooled, and interest rates went up. If Zillow, with all its billions invested and access to plenty of consumer data, couldn’t get this right, traditional property developers and brokers may find it challenging.”

Q: Developers often face large volumes of unsold inventory while buyers struggle with affordability. From your perspective, what structural mismatches between pricing, financing, and buyer education are driving this paradox?

Faizul Ridzuan: It is a fundamental mismatch of supply and demand. What is being built doesn’t always match what people want, or at least, not at a price they can afford. The litmus test for using the right data is simple: 80% sales in the first year. If a developer launches 1,000 units and fails to sell 800, they haven’t just had a bad sales quarter; they’ve fundamentally misread the market.

Anything less than 80% usually means the developer’s calculations are wrong. It is rarely a sales execution problem; it is almost always a product-market fit problem. The size and price must align with the area’s median affordability. If you hit that sweet spot, financing can fall into place naturally. Education isn’t the deciding factor here; the product is.

80% is the magic number. Achieving this means the project hits breakeven early, killing negative cash flow and drastically reducing the risk of delays or abandonment. The developer can focus on building, rather than worrying about chasing sales three years post-launch.

At the right price point, valuations hold up, sales convert faster, and banks are happy because the Non-Performing Loan (NPL) risk drops significantly. When you use the right data to design the supply, it’s a win for the developer, the bank, and the buyer.

Q: FAR Capital sits between buyers, banks, and developers. Who ultimately pays you, how are incentives aligned across all parties, and where do conflicts of interest typically arise in this ecosystem?

Faizul Ridzuan: Continuing from that, the entire strategy hinges on using the right data to increase the likelihood that developers build the right property at the right size. The moment a project is abandoned due to a supply-demand mismatch, usually stemming from wrong data, everyone is affected. We directly serve two parties, developers and buyers, and both contribute to our compensation. When a project completes successfully, the banks naturally win. The proof is in the numbers: over the last 10 years, our NPL rate is less than 0.02%. That is almost 50 times lower than the market average. You could argue that we have helped lower the bank’s NPL, indirectly.

Ultimately, if we have to pick a side, our main customer is the property buyer. We consistently provide the properties they need at the right price point, which drives our very healthy repeat purchase rate. Our goal has always been to engineer a safe property ecosystem where developers, banks, and buyers can build, finance, and buy with confidence. This year, we are targeting to help developers launch about 3,000 units, and we are optimistic we can help secure 80% sales for them in the first 12 months of launch using this proven methodology.

Q: You emphasize zero-down or minimal-capital property acquisition. In a rising-rate environment, how do you manage clients being over-leveraged, and where do you draw the line between opportunity and excessive risk?

Faizul Ridzuan: The inefficiency is the massive gap between retail pricing and wholesale cost. When a developer sells individually, they bleed money on exorbitant marketing campaigns, fancy sales galleries, and agent commissions. That is 15–20% of the GDV wasted right there. We solve this with volume. We bring 50, 100, or even 200 credit-worthy buyers to the table at once. In exchange, we demand the developer strip out those marketing costs and pass that value directly to our clients.

Traditional brokers can’t do this; they don’t have the volume. Developers are a skeptical bunch; most are addicted to the retail model. We simply industrialized bulk buying. If you buy one shirt, you pay retail. If you buy 5,000 shirts, you pay wholesale. We are the Costco of property buying; we aggregate demand to force supply prices down.

This aggregate buying power is exactly how we accomplish “Zero-down.” If a developer wants $500,000 for a unit, that is the base price for one buyer. But when FAR Capital negotiates to buy 50 units, the price can drop to $450,000. Logic dictates that buying at $450,000 is inherently less risky than buying the exact same property at $500,000. That instant equity buffer is one of the main reasons our NPL rates are so low. When you buy the right property at the right price point, it helps protect you and gives you a much higher margin of safety.

Q: Malaysia has relatively high homeownership alongside growing affordability stress. Which market conditions make FAR Capital viable here, and which of those conditions would need to exist for the model to scale to other geographies?

Faizul Ridzuan: FAR Capital thrives where the demographics are hungry. We need three specific conditions: a young population averaging under 35 where ownership is below 50%, a rising middle class with real income growth, and consistent GDP growth of at least 3% year-on-year.

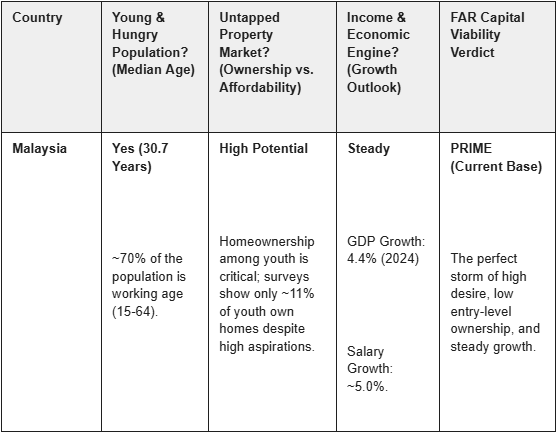

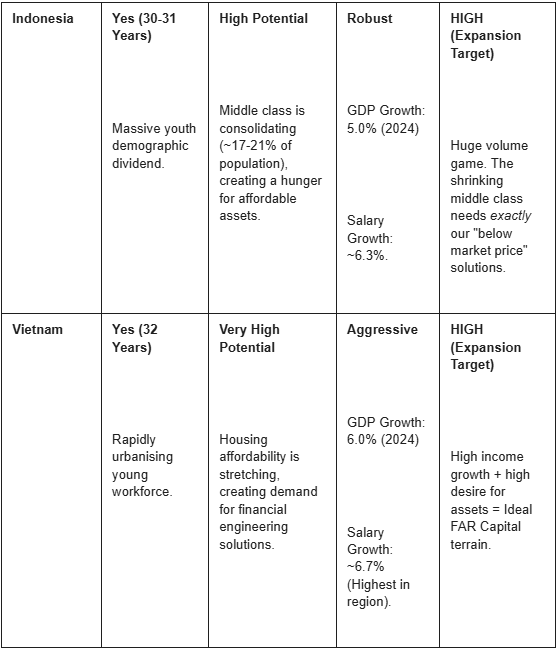

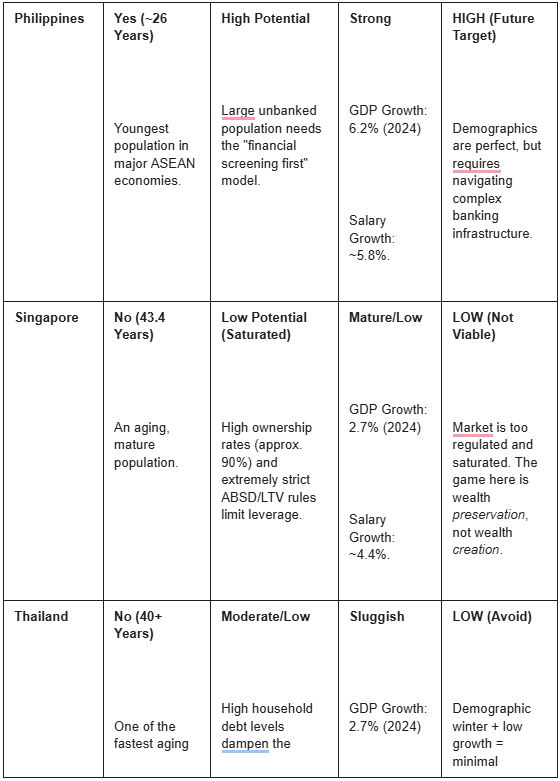

Long story short, developing markets are our playground. In developed markets, the game is set. In markets like Malaysia, Indonesia, and Vietnam, the game is still being written, and our model is the pen. The data below illustrates why we are betting on these specific “Blue Ocean” markets over mature ones like Singapore or stagnation-prone ones like Thailand.

The data below proves exactly why we are betting on these specific “Blue Ocean” markets over mature ones like Singapore or stagnation-prone ones like Thailand.

ASEAN Market Viability Matrix

Analyst Note: The data clearly bifurcates ASEAN.

Malaysia, Indonesia, Vietnam, and Philippines are “Green Zones” with young populations (median age <35) and high growth (>4% GDP), fitting the FAR Capital model perfectly.

Singapore and Thailand are “Red Zones” – aging, slower growth, or highly saturated, making them unsuitable for a high-leverage, mass-market acquisition strategy.

Disclaimer: The content is intended for informational purposes only and does not constitute financial or investment advice. Readers are encouraged to consult with a qualified professional before making any financial decisions.